Over the last several months, wheat prices have been a roller coaster. Fertilizer

supply concerns from the Iran Conflict and degrading growing conditions in the central

Great Plains pushed Chicago Mercantile Exchange winter wheat futures prices from $5.75

per bushel in late February to $7.50 in the middle of May. Futures have now settled

at roughly $6.25 per bushel. With this intense price volatility, it’s easy for growers

to focus on the exchange price above all else, but it’s important not to lose track

of what’s happening at the local elevator—both through cash prices and basis.

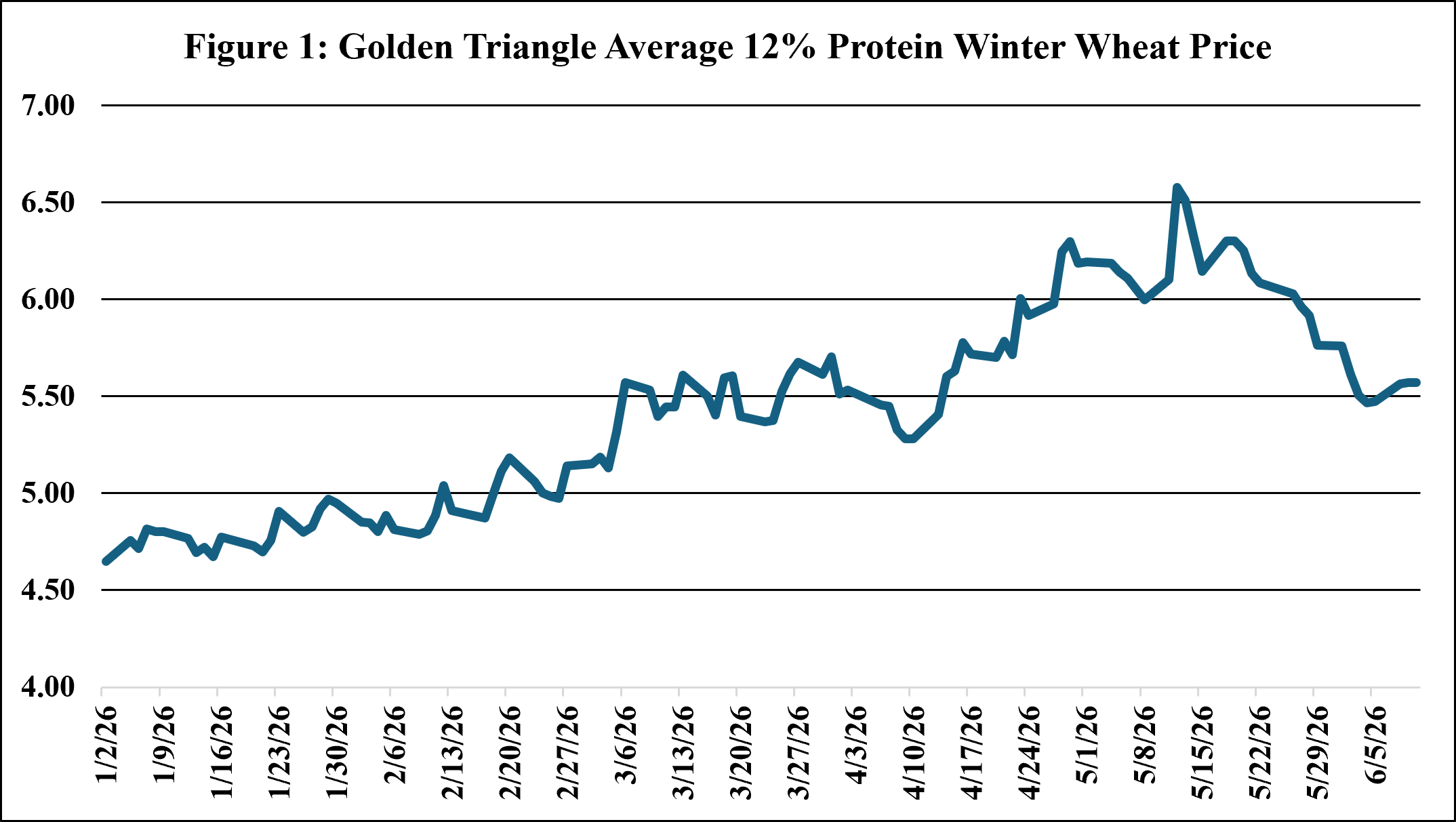

So, what’s been happening with local cash grain prices? Figure 1 below shows the average

price for hard red winter wheat in the Golden Triangle region of Montana. Prices have

steadily increased throughout the year, and at the start of the Iran conflict in early

March, local prices jumped by almost $0.50 per bushel. Concerns about yield in the

Great Plains helped push cash prices towards $6.50 per bushel in the middle of May,

but prices are now closer to $5.50 per bushel.

Source: (USDA-AMS, 2026)

However, cash prices only tell part of the story. Local cash grain bids reflect both

national supply and demand conditions through the futures price, and they also reflect

local supply and demand conditions through basis. Basis is the difference between

the local cash price and the futures contract closest to expiration. For example,

if the current local cash price is $5.50 per bushel and if the futures contract with

the nearest expiration date is $6.00 per bushel, then basis is -$0.50 per bushel ($5.50-$6.00=-$0.50).

Keeping track of basis can help farmers better understand local factors affecting

their cash wheat prices.

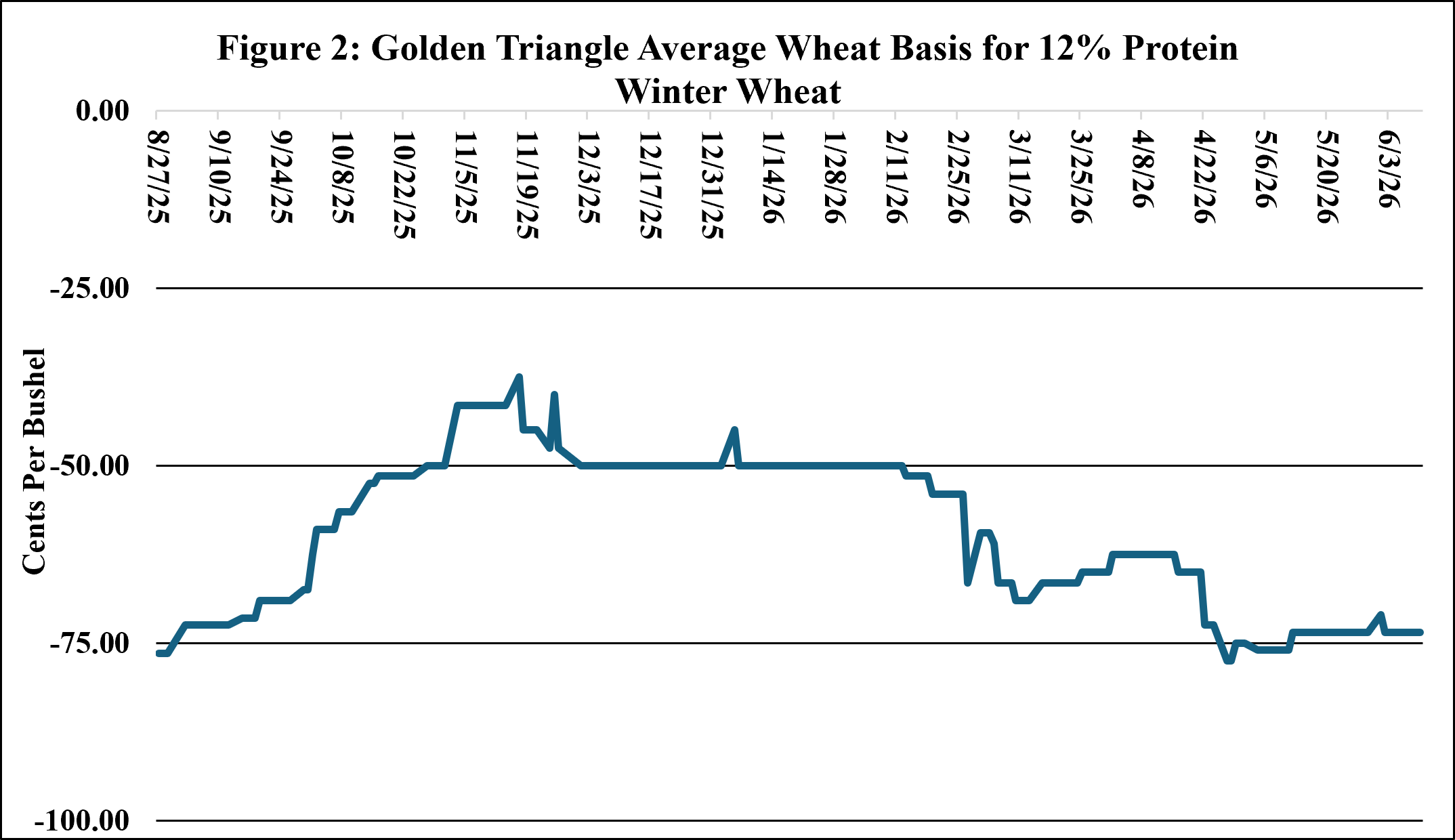

Figure 2 shows the average basis for 12% protein winter wheat in the Golden Triangle

region since the Montana harvest of 2025. Basis tends to cycle with the marketing

year. Farmers usually see the lowest basis right around harvest, as this is when local

supply is at its greatest. Basis then tends to strength as local wheat supplies are

moved out of the region to mills or to export markets along the coast of Washington

until next year’s harvest starts the cycle again. Basis during 2025’s harvest was

quite weak at -$0.75 per bushel, but it steadily improved to -$0.50 per bushel.

Source: (USDA-AMS, 2026)

However, since the start of the Iran War, basis has significantly weakened back to

-$0.75 per bushel. This downward trend in basis has limited the benefits to local

farmers from the recent price rally in the futures market.

So, what’s driving the movement in wheat basis? Global supplies for wheat reached

their highest levels in six years following 2025 harvests. These high supplies sent

prices lower, but the United States experienced strong export demand following the

2025 harvest. In September 2025, the United States exported 3.25 million metric tons

of wheat—30% higher than September 2024 (USDA-GATS, 2026). These exports helped to

strengthen local basis by moving local supplies out of the Pacific Northwest region.

However, export demand for US wheat has since slowed with April 2026 export volumes

below volumes in April of 2024 and 2025. Near record harvests in Argentina and Australia

created greater competition for export. Likewise, the Iran War has thrown global shipping

into chaos, increasing costs for grain exporters. In March 2026, the USDA reported

the highest wheat stocks for the state of Washington since 2021. Concerns over yields

in the Great Plains, could start another futures price rally. However, until export

demand picks back up, local stocks will likely continue to be above average through

the rest of the 2025-2026 marketing year, putting pressure on basis.

Andrew Swanson

Assistant Professor

Montana State University is an ADA/EO/AA/Veteran’s Preference Employer and Provider of Educational and Outreach.